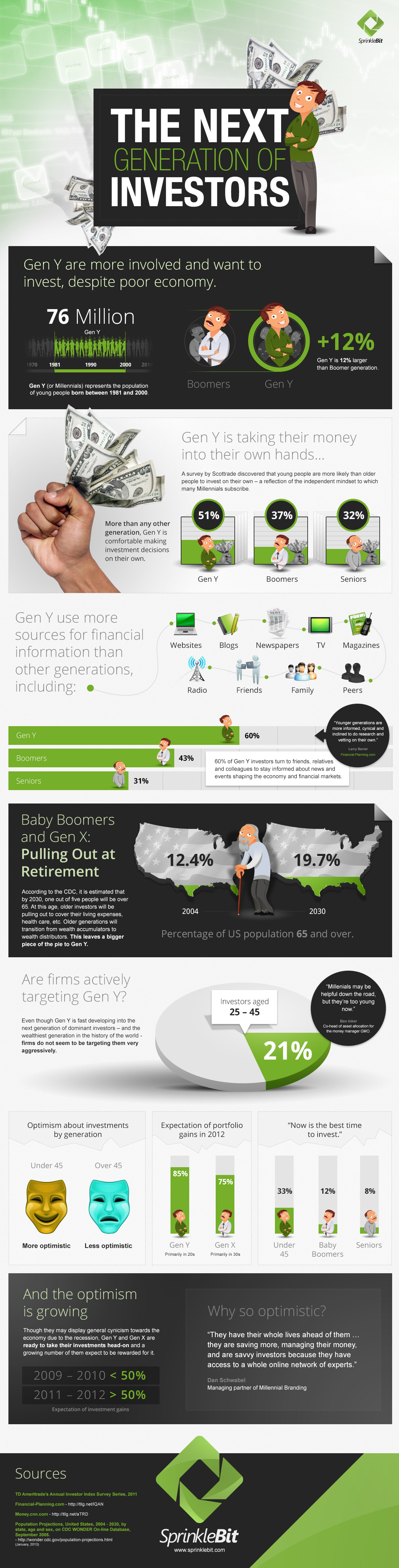

Gen Y: The Next Generation of Investors

Move over Baby Boomers, the next generation of investors is here and they plan on doing big things. With Gen Y youth (born between 1981 and 2000) coming to an earning stage of their lives, it is worth noting that they behave differently from investors of the previous generations. Gen Y, also known as Millennials, have grown up with the abundance of quality and timely information always within an arm’s reach. Young investors today use multiple sources of information that were not available to previous generations to make informed financial decisions. Therefore, investors of this era have become more independent and are inclined to perform research for their investments and finances on their own. Side note: This is why we created Visual Capitalist. We want to inform the modern investor as quickly and efficiently as possible as they are inundated with a myriad of information every moment of every day. We believe visual learning is the best way to consume and retain useful information. As Baby Boomers, and eventually Gen X, start to age and pull their investments to cover cost of retirement, more investment opportunities are opening up for Gen Y. In America, almost 20% of the population will be over the age of 65 by 2030. The older generation will go from being “wealth accumulators” to “wealth distributors”. The economic collapse in the late 2000s led many young people to see their parents’ financial well-being fall apart. The newest generation of investors has learned that they need to be smart with their money and stay ahead of the game to avoid a similar fate. Source: Sprinklebit blog – The Next Generation of Investors on Last year, stock and bond returns tumbled after the Federal Reserve hiked interest rates at the fastest speed in 40 years. It was the first time in decades that both asset classes posted negative annual investment returns in tandem. Over four decades, this has happened 2.4% of the time across any 12-month rolling period. To look at how various stock and bond asset allocations have performed over history—and their broader correlations—the above graphic charts their best, worst, and average returns, using data from Vanguard.

How Has Asset Allocation Impacted Returns?

Based on data between 1926 and 2019, the table below looks at the spectrum of market returns of different asset allocations:

We can see that a portfolio made entirely of stocks returned 10.3% on average, the highest across all asset allocations. Of course, this came with wider return variance, hitting an annual low of -43% and a high of 54%.

A traditional 60/40 portfolio—which has lost its luster in recent years as low interest rates have led to lower bond returns—saw an average historical return of 8.8%. As interest rates have climbed in recent years, this may widen its appeal once again as bond returns may rise.

Meanwhile, a 100% bond portfolio averaged 5.3% in annual returns over the period. Bonds typically serve as a hedge against portfolio losses thanks to their typically negative historical correlation to stocks.

A Closer Look at Historical Correlations

To understand how 2022 was an outlier in terms of asset correlations we can look at the graphic below:

The last time stocks and bonds moved together in a negative direction was in 1969. At the time, inflation was accelerating and the Fed was hiking interest rates to cool rising costs. In fact, historically, when inflation surges, stocks and bonds have often moved in similar directions. Underscoring this divergence is real interest rate volatility. When real interest rates are a driving force in the market, as we have seen in the last year, it hurts both stock and bond returns. This is because higher interest rates can reduce the future cash flows of these investments. Adding another layer is the level of risk appetite among investors. When the economic outlook is uncertain and interest rate volatility is high, investors are more likely to take risk off their portfolios and demand higher returns for taking on higher risk. This can push down equity and bond prices. On the other hand, if the economic outlook is positive, investors may be willing to take on more risk, in turn potentially boosting equity prices.

Current Investment Returns in Context

Today, financial markets are seeing sharp swings as the ripple effects of higher interest rates are sinking in. For investors, historical data provides insight on long-term asset allocation trends. Over the last century, cycles of high interest rates have come and gone. Both equity and bond investment returns have been resilient for investors who stay the course.